b2b Commercial Card Acceptance: Add Six Figures to Your Revenue

AI Overview

Intro to B2B Payments 2025 and Beyond

In today’s fast-moving B2B economy, the way you accept payments is no longer just a back-office decision. It’s a strategic driver of growth, cash flow, and customer satisfaction.

Yet many businesses remain hesitant to accept commercial credit cards, assuming the merchant discount rate (MDR) and processing fees will eat into their margins.

But the data tells a different story.

According to a Forrester Total Economic Impact™ (TEI) study commissioned by Visa, companies that accept commercial credit cards see a 132% ROI, with payback in under six months. The study found that card acceptance drives revenue lift, improves collections, reduces fraud, and streamline operations. (Read the full Forrester study here).

So, what does that mean for mid-market businesses doing $2M–$10M a year in sales? Let’s break it down.

sponsored by

Modeling the Impact: 50% Card Adoption

Forrester’s $10B composite enterprise model is useful, but let’s apply the same framework to a smaller company.

Using region-average benchmarks:

- Incremental Sales Lift: +100 basis points (1.00%)

- Net Benefits (Operational & Financial Gains): +62.5 basis points (0.625%)

- Total: +162.5 BPS (1.625%)

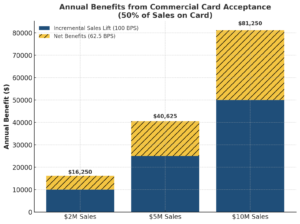

📊 Infographic: Benefits by Revenue Size

What the numbers show:

- $2M annual sales → ~$32,500 annual benefit

- $5M annual sales → ~$81,250 annual benefit

- $10M annual sales → ~$162,500 annual benefit

The stacked bars represent:

- Incremental Sales Lift (100 bps): More sales volume and larger orders because customers prefer paying by card.

- Net Benefits (62.5 bps): Faster collections, lower bad debt, reduced AR costs, and better working capital.

Even modest adoption can unlock six-figure value. For mid-market companies, this isn’t just about offsetting card fees—it’s about driving predictable growth and stronger cash flow.

Why Businesses Benefit from Accepting Cards

-

Revenue Growth

Buyers increasingly expect card options, especially hospitals, private equity-backed firms, and enterprises that earn rebates or need expense tracking. Accepting cards reduces friction and prevents lost business to competitors.

-

Better Debt Collection

Forrester found a 20% improvement in collections because cards allow immediate settlement and eliminate reliance on slow checks or third-party agencies.

-

Faster Cash Flow

Switching to cards can cut Days Sales Outstanding (DSO) from 30–45 days down to 15–18 days. That means more predictable working capital and less borrowing to cover receivables.

-

Operational Efficiency

Card payments reduce manual AR work like reconciliations, fraud affidavits, and exception handling. Finance teams can focus on strategy instead of chasing checks.

-

Customer Experience

Offering flexible, modern payment options builds loyalty. Customers prefer convenience, and many actively seek suppliers who accept cards.

NPS Advantage: ACH + Flexible Pricing Models

At Nationwide Payment Systems, we know one size doesn’t fit all. That’s why our platform goes beyond card acceptance with options designed to maximize choice and savings:

-

Integrated ACH Payments:

Give your customers flexibility to pay by card or ACH, depending on their preferences and your business rules. ACH offers low-cost electronic transfers that work especially well for repeat B2B buyers.

-

Surcharge, Dual Pricing, and Convenience Fees:

Offset or eliminate card acceptance costs by passing fees transparently. Whether it’s dual pricing at the register, surcharging for card use, or convenience fees for online payments, these tools help you keep more of your margin.

-

ClickBillR + NPSOne Integration:

Combine invoicing, card, and ACH acceptance with flexible pricing options in one seamless platform.

-

Flexible API:

You can also integrate our gateway into your software! And we will create a test account, with Slack and technical support assigned to help you get the project finished fast!

This means your business gets the benefits of card acceptance without the margin pressure—because you control how costs are managed and how customers pay.

Connecting to the Forrester TEI Study

In Forrester’s $10B composite enterprise model, companies that accepted commercial credit cards saw:

- $175M in incremental revenue over three years

- $157.8M in improved debt collection

- $11.9M from reduced DSO

- $5.7M from process efficiencies

Even after costs (transaction fees and internal resources), the net profit was 420 basis points per transaction. (Full study PDF).

This framework provides a proven model to benchmark your own numbers against.

Use the Visa B2B Card Value Calculator

Want to test this with your own revenue? Visa offers a free, interactive calculator where you can plug in your sales, margin, and card adoption rate. It will estimate your potential incremental benefits.

👉 NPS B2B CARD VALUE CALCULATOR

Final Thoughts

The old argument that “card fees are too expensive” doesn’t hold up under scrutiny. In reality, accepting commercial credit cards improves revenue, accelerates cash flow, reduces bad debt, and creates efficiencies that are more than offset costs.

And with Nationwide Payment Systems, you get even more leverage:

- Accept both cards and ACH in one platform.

- Deploy surcharge, dual pricing, or convenience fees to offset costs.

- Use ClickBillR and NPSOne for seamless invoicing, online payments, and reporting.

For a $10M company, switching 50% of sales to commercial cards can yield over $160,000 in incremental annual benefit. Even a $2M firm could unlock over $30,000.

If you want to see how this could work for your business, start with two steps:

- Review the Forrester TEI Study for detailed benchmarks.

- Use the Visa B2B Card Value Calculator to model your own impact.

At Nationwide Payment Systems, we’re here to help you implement the right mix of card + ACH acceptance and flexible pricing models to maximize ROI.

👉 Book a consultation with us today and learn how we can help optimize your B2B payments strategy.

CLICK HERE TO FIND MORE ABOUT OUR PROGRAMS

FAQ: Frequently Asked Questions

Aren’t card fees too high to make this worthwhile?

Not when you look at net impact. Forrester found that benefits outweighed costs by 132% ROI over three years.

Does this only work for large enterprises?

No. As our $2M–$10M example shows, even mid-sized businesses can see five- to six-figure annual benefits.

What if my customers don’t want to use cards?

Start with a pilot program. Many buyers prefer cards once they see the convenience, rewards, and faster settlement.

How quickly do businesses see payback?

The Forrester study found average payback in under six months.

What about fraud or chargebacks?

Commercial card transactions are highly secure, with real-time monitoring and protections not available with checks.

Does this replace ACH or checks?

No—it complements them. With NPS, you can accept both cards and integrated ACH to maximize flexibility.

How much can DSO improve?

In many cases, DSO is reduced by two-thirds—for example, from 30 days down to 10–15.

What about customers with strict payment terms?

Offering multiple options—including ACH and card with flexible pricing models—lets you align terms with customer needs while protecting your margins.

Are internal costs significant?

Implementation requires some effort, but efficiency gains offset this quickly. Forrester found internal costs modest compared to benefits.

How can I build a business case for leadership?

Use Forrester’s ROI benchmarks plus Visa’s calculator. Show your current payment mix vs. a card adoption scenario, and layer in ACH and dual pricing to demonstrate maximum savings.